Multi-Asset Investments Views: Welcome to a new kind of tension

- 27 February 2025 (7 min read)

KEY POINTS

Less than two months into President Donald Trump's return to the White House (though it may feel longer, given the number of announcements already witnessed), his policy agenda is closer to that of the second year of his first term.

The administration is focusing on tariffs, as it did in mid-2018, rather than on deregulation and fiscal stimulus. Moreover, uncertainty over policy is generating a new kind of tension for financial markets, with tariffs announced as imminent and unavoidable, then postponed, with the order of countries being targeted continuing to change. Asset prices have been mirroring the back-and-forth of headlines, Presidential phone calls and tweets, as investors appeared to have to second-guess whether Trump’s aggressive approach to policy is ultimately transactional or dogmatic.

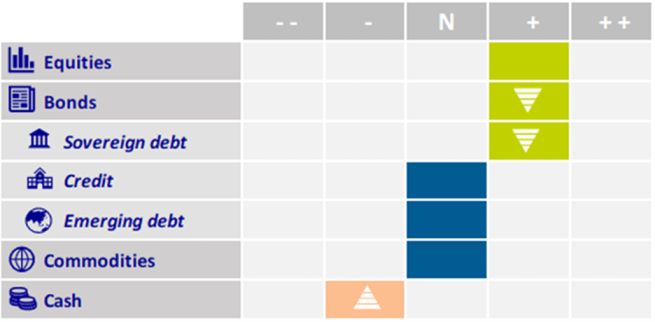

Perhaps counter-intuitively, active portfolio management means holding onto a stable medium-term conviction above and beyond the short-term volatility. From that perspective, we remain modestly optimistic with our main outlook still a combination of (limited) disinflation and resilient economic growth. However, markets have been flirting with what we call the ‘danger zone’, in which high interest rates hurt equity valuations - we are currently just on the positive side of that zone.

Within equities, the start of this year saw a rare underperformance of the US market compared to the rest of the world. The notable outperformance of European equities was in part attributed to some fundamental improvements.

The Eurozone Economic Surprise Index moved into positive territory in February, indicating that macroeconomic indicators released over the past month have hit their best level in a year. A similar optimism emerged across many European corporates, as the most recent quarterly earnings results once again beat expectations. Investor sentiment also ticked up, with some potential positive catalysts on the horizon; from a possible Ukraine ceasefire to fiscal stimulus from Germany and China (the latter helping many export-driven European businesses).

In our view, the largest contributor to this absolute and relative performance of European equities was positioning: the overwhelming ‘US Supremacy’ narrative of recent years had left many investors underweight in Europe. In October 2024, markets reached an extreme positioning of maximum net long on the US and net short on Europe.

Now, the positioning has not only reversed but flipped altogether: investors now hold greater proportional overweight positions in Europe (on a normalised basis) than in the US. While the positioning is not yet stretched, the profit that has built up is extended, adding an element of risk in that any potential correction could be amplified by investors who hold overweight positions taking profits.

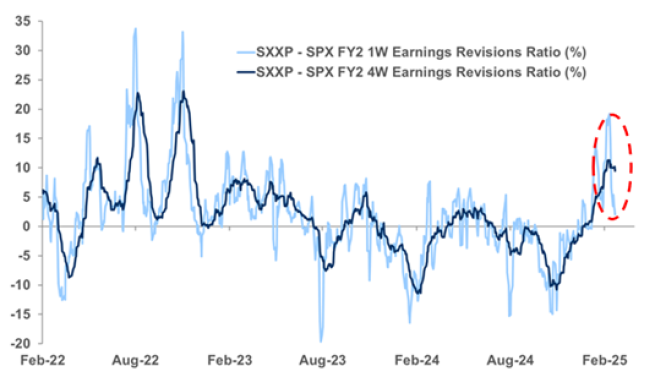

With US earnings revisions having likely bottomed (see chart below), we favour the US within our equity allocation, with a preference for quality names and for deregulation-boosted industries, such as financials and technology companies.

We also increased our tactical exposure to Chinese equities. The fundamental view of our macroeconomic outlook remains gloomy: the Chinese economy has suffered for several years from deflation and the housing debt hangover. Our move is due to a change in market sentiment, buoyed by a low positioning starting point.

Indeed, the Chinese authorities have recently radically changed their stance on the private sector, turning to a much more pro-growth narrative. To some, President Xi Jinping’s words - that it would now be “acceptable for top private executives to prosper first” - were reminiscent of former President Deng Xiaoping’s theory on opening up to capitalism. Meanwhile, the emergence of artificial intelligence start-up DeepSeek reignited interest in China tech stocks which still trade at a significant discount to their US peers.

On the fixed income side, German and Eurozone yields have recently underperformed their US equivalent: the 10-year Bund interest rate fell below 2.4% before rising more than 15 basis points in only a week. We still favour Eurozone bonds, on the back of the region’s weaker growth outlook and the European Central Bank’s (ECB) comparatively dovish stance.

Yet, we are mindful that any real increase in European defence spending would demand deeper deficits and a higher term premium for European bonds, while higher-for-longer US Treasury yields have been lifting Eurozone interest rates since the third quarter of 2024 and continue to do so.

Altogether, we have marginally reduced the interest-rate sensitivity of our portfolios. Disinflationary forces from energy and food prices in the event of a resolution to the war in Ukraine will likely support yields on short-term bonds and force the ECB’s hand.

Disclaimer

This website is published by AXA Investment Managers Australia Ltd (ABN 47 107 346 841 AFSL 273320) (“AXA IM Australia”) and is intended only for professional investors, sophisticated investors and wholesale clients as defined in the Corporations Act 2001 (Cth).

This publication is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Market commentary on the website has been prepared for general informational purposes by the authors, who are part of AXA Investment Managers. This market commentary reflects the views of the authors, and statements in it may differ from the views of others in AXA Investment Managers.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk , including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested.