How regulatory momentum is helping drive biodiversity-aware investment

- 09 May 2023 (5 min read)

Key points:

- Biodiversity is a deeply complex topic with a host of potential actions and consequences. The regulatory response so far is reflective of that

- From the Convention on Biological Diversity to the Global Biodiversity Framework and a series of measures at EU and local level, regulation – and the definitions and data that underpin it – are becoming more robust

- We expect this process to continue, and to offer a potential advantage to the best-prepared companies and investors

Investments that take account of environmental, social and governance (ESG) factors have always gone hand-in-hand with public policy. As investors become increasingly aware of the potential financial effects of climate change, so too regulators begin to impose demands that echo the concerns and may harden those financial effects on asset prices. The same is true of biodiversity: Regulation both reflects and drives momentum alongside our growing understanding of its economic importance.

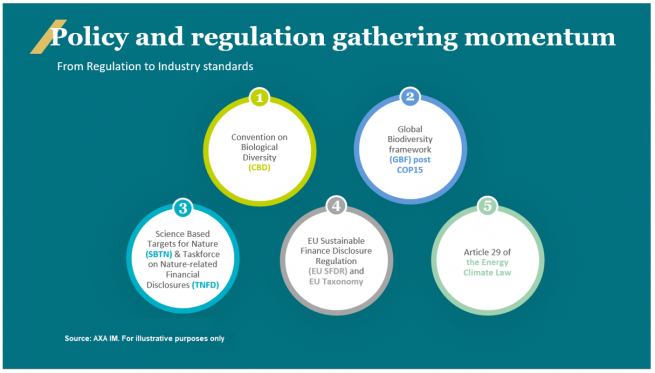

Biodiversity is a deeply complex topic with multiple strands and a host of potential solutions and consequences. As such, the regulatory response is also multi-layered, built on decades-old global guidelines, invigorated by brand new local initiatives and enhanced by an ever-improving grasp of how investors and companies can measure and track their impact. Below, we introduce five key elements that we believe are defining the corporate and investment world’s response to biodiversity loss.

Convention on Biological Diversity

The Convention on Biological Diversity (CBD) is the cornerstone of the global response to biodiversity loss – an international legal instrument agreed in the early 1990s and ratified by every United Nations member state apart from the US.1 Its importance has ebbed and flowed in the meantime, but its influence has revived in recent years as the issue gains prominence. Its overarching objective is to help develop national strategies for the conservation and sustainable use of biological diversity.

The CBD has been supplemented by two other agreements, the 2000 Cartagena Protocol that addressed the movement of genetically modified organisms between countries and the 2010 Nagoya Protocol which seeks to ensure fair use and sharing of genetic resources, such as medicines derived from indigenous plants.

The CBD sets out agreed global definitions for biological diversity, ecosystems, habitat and so on, as well as for what is deemed “sustainable use” of natural resources. It also calls for global cooperation in implementation of conservation and incentive measures and puts the focus on the importance of eventual financial mechanisms to support global nature protection objectives.

Global Biodiversity Framework

Adopted in December 2022 at the United Nations (UN) COP15 biodiversity conference, this agreement reinforces the global framework on biodiversity set by the CBD. It provides guidance on the collective targets for countries, companies and financial institutions as well as on the actions needed to achieve those targets.2 Known as the Kunming-Montreal Global Biodiversity Framework (GBF), the deal was signed by 196 countries that have committed to “take urgent action to halt and reverse biodiversity loss” by 2030 – specifically to protect 30% of land and sea area by that date.

It is not a legally binding document but we think it is very likely to guide and drive policy action that will have implications for businesses and investors. Signatory nations are committed to setting national targets to implement the framework and are required to show progress towards them and to update National Biodiversity Strategies and Action Plans accordingly.

And so, we expect the GBF to accelerate the enhancement and adoption of indicators for tackling biodiversity loss, and we expect it to drive greater global harmonisation of regulatory demands and policies around sustainable finance. Most relevant for investors, we anticipate nature-related disclosure and data to become mandatory for companies and eventually for financial institutions, and that biodiversity targets and due diligence obligations will follow. The GBF explicitly states financial companies should report on this too.

It will be important for investors, and particularly pension funds and insurers, to adapt quickly in this rapidly changing environment. The GBF targets are just seven years away, and we think institutional investors should be taking urgent steps to ensure their portfolios are fit for purpose. The first results of actions to align with the framework’s targets will be expected by the next meeting of the UN Biodiversity Conference, COP16, in Turkey in 2024.

Taskforce on Nature-related Financial Disclosures

This sister project to the Taskforce on Climate-related Financial Disclosures (TCFD) is placing new demands on businesses to acknowledge and disclose the risks related to biodiversity loss in their operations.3 The final version is expected in September this year.

The Taskforce on Nature-related Financial Disclosures (TNFD) is expected to play the key role in defining those mandatory data and disclosures that form part of the GBF commitments, alongside work carried out by the Science Based Targets for Nature initiative. Consistent, agreed measurement standards remain difficult areas in biodiversity, and will likely remain more complex than for climate, where carbon emissions and intensity are useful catch-all datapoints.

AXA IM’s parent company, AXA Group, was one of the initiators of the TNFD in 2020. This industry-led group will deliver a risk management and disclosure framework for organisations to report and act on evolving nature-related risks. Although its guidelines may be applied widely across the corporate world, there is a focus on financial institutions, with the ultimate goal of supporting a shift in global capital flows away from nature-negative outcomes and toward nature-positive outcomes.

By providing a common reporting framework on nature impacts, dependencies, risks and opportunities for financial institutions, the TNFD should help provide incentives for a reduction of impacts on nature and transition towards less nature-intensive economies globally. As with the TCFD, the TNFD is an industry-led initiative, which national or regional policymakers may in due course choose to leverage.

The EU’s Sustainable Finance Disclosure Regulation

While the CBD and GBF remain non-binding, the European Union’s (EU) broad set of rules designed to improve transparency in the market for sustainable investment products also includes specific reference to biodiversity risks.

The Sustainable Finance Disclosure Regulation’s (SFDR) mandatory Principal Adverse Impact (PAI) indicator on the issue requires that companies disclose activities that may damage biodiversity. It is one of 18 PAIs and will seek to address the difficulties around biodiversity data by using a practical approach that calculates the share of investments in companies with sites or operations that are located in or near to biodiversity-sensitive areas, or which negatively affect those areas.

The SFDR is not the EU’s only tool in its efforts to tackle biodiversity loss. It has introduced a plan to halve pesticide use by 2030 and restore 80% of damaged European habitats by 2050, as well as a separate legislative proposal designed to tackle global deforestation and forest degradation.4 , 5

In addition, the European Commission’s sustainable finance experts recently published a consultation on draft technical recommendations for the non-climate environmental objectives of the EU Taxonomy of green activities.6 Among those objectives is biodiversity protection. We expect the EU Taxonomy – which aims to set out classifications that restrict what can be claimed about environmental impacts – to play an important role in the definition of nature-positive businesses in the future.

France’s Article 29

A good example of how these global and supranational efforts may feed into local initiatives is seen perhaps most clearly in French regulation – notably in Article 29 of the Law on Energy and Climate. This requires French financial institutions to clearly disclose their strategy for reducing biodiversity impacts, including specific targets and reference to how those efforts align with the CBD.

They are also required to identify impacts on biodiversity related to investments and disclose how investments may contribute to reducing those biodiversity impacts, in line with the Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES) as well as with the global goals and guidelines, including the CBD. For this, the regulation states that financial institutions may use a biodiversity footprint indicator when applicable.7 They must also report on how biodiversity is considered in their shareholder engagement and stewardship activities.

France can be argued to have led the way on climate-related disclosures, and we would expect to see many of the demands set out in Article 29 being incorporated into legislation elsewhere.

A common purpose

How these initiatives, guidelines and regulations interact is a work in progress. There is little thus far in the way of definitive, binding obligations on investors, but clearly there is a powerful momentum towards policy and regulatory measures that ask us to define and report our collective impact on biodiversity.

Importantly, we believe that this momentum – alongside biodiversity’s link to least five of the UN Sustainable Development Goals – has already helped create a transition opportunity for businesses in different industries that investors may want to support. There is a growing sense of common purpose towards quality data and measurement techniques that could eventually inform and influence allocations. We think this evolution in how we understand our effect on the natural world may potentially reward players that proactively undertake a nature-positive transition in the corporate world, as well as favouring investors taking the time to build their expertise and integrate biodiversity into investment decision-making.

- RnVsbCBUZXh0IG9mIHRoZSBDb252ZW50aW9uIG9uIEJpb2xvZ2ljYWwgRGl2ZXJzaXR5LCBDQkQsIE1heSAyMDE2IHVwZGF0ZQ==

- S3VubWluZy1Nb250cmVhbCBHbG9iYWwgQmlvZGl2ZXJzaXR5IEZyYW1ld29yaywgQ0JELCBGZWJydWFyeSAyMDIz

- SW50cm9kdWNpbmcgdGhlIFRORkQgZnJhbWV3b3JrLCBUTkZELCByZXRyaWV2ZWQgTWF5IDIwMjM=

- R3JlZW4gRGVhbDogcGlvbmVlcmluZyBwcm9wb3NhbHMgdG8gcmVzdG9yZSBFdXJvcGUncyBuYXR1cmUgYnkgMjA1MCBhbmQgaGFsdmUgcGVzdGljaWRlIHVzZSBieSAyMDMwLCBFdXJvcGVhbiBDb21taXNzaW9uLCBKdW5lIDIwMjI=

- UmVndWxhdGlvbiBwcm9wb3NhbCBvbiBkZWZvcmVzdGF0aW9uLWZyZWUgc3VwcGx5IGNoYWluczogbWluaW1pc2luZyB0aGUgcmlzayBvZiBkZWZvcmVzdGF0aW9uIGFuZCBmb3Jlc3QgZGVncmFkYXRpb24gYXNzb2NpYXRlZCB3aXRoIHByb2R1Y3RzIHBsYWNlZCBvbiB0aGUgRVUgbWFya2V0LCBFdXJvcGVhbiBDb21taXNzaW9uLCBEZWNlbWJlciAyMDIx

- RVUgdGF4b25vbXkgZm9yIHN1c3RhaW5hYmxlIGFjdGl2aXRpZXMsIEV1cm9wZWFuIENvbW1pc3Npb24sIHJldHJpZXZlZCBNYXkgMjAyMw==

- SWNlYmVyZyBEYXRhIExhYiBwcm92aWRlcyBhIENvcnBvcmF0ZSBCaW9kaXZlcnNpdHkgRm9vdHByaW50IChDQkYpIG1ldHJpYyB0aGF0IGlzIGV4cHJlc3NlZCBpbiBzcXVhcmUga2lsb21ldHJlcyAoa23Csikgb2YgbWVhbiBzcGVjaWVzIGFidW5kYW5jZSAoTVNBKSDigJMgYSByZWNvZ25pc2VkIHByb3h5IGZvciB0aGUgaW50YWN0bmVzcyBvZiBiaW9kaXZlcnNpdHkgY29tcGFyZWQgdG8gYSBwcmlzdGluZSwgdW5kaXN0dXJiZWQgc3RhdGUuIENCRiBkYXRhIGlzIGN1cnJlbnRseSBhbG1vc3QgZW50aXJlbHkgbW9kZWxsZWQgYW5kIGludGVncmF0ZXMgb25seSBzb21lIG9mIHRoZSBmaXZlIHByaW1hcnkgZHJpdmVycyBvZiBiaW9kaXZlcnNpdHkgbG9zcyBhcyBkZWZpbmVkIGJ5IElQQkVTLiBJdCB0aGVyZWZvcmUgcHJvdmlkZXMgYSBwYXJ0aWFsIHBpY3R1cmUgb2YgZWZmZWN0aXZlIGltcGFjdHMgYW5kIHJpc2tzLiBUaGUgZGF0YSBhbmQgbW9kZWwgd2lsbCBjb250aW51ZSB0byBldm9sdmUgaW4gdGhlIGZ1dHVyZS4gQVhBIElNIGlzIGEgc2hhcmVob2xkZXIgaW4gSWNlYmVyZyBEYXRhIExhYi4=

Read more on biodiversity

Biodiversity Q&A: Understanding a powerful new investment theme

Shifting the natural cost curve: The role of investors in protecting biodiversity

Why investing in biodiversity means looking at the solutions, not just the problems

Why, and how, investors should integrate biodiversity into fixed income portfolios

Brazil: Lula 3.0 – Good news for climate and biodiversity?

Feeding the world and protecting the planet: A biodiversity and climate challenge for investors

Disclaimer

This website is published by AXA Investment Managers Australia Ltd (ABN 47 107 346 841 AFSL 273320) (“AXA IM Australia”) and is intended only for professional investors, sophisticated investors and wholesale clients as defined in the Corporations Act 2001 (Cth).

This publication is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Market commentary on the website has been prepared for general informational purposes by the authors, who are part of AXA Investment Managers. This market commentary reflects the views of the authors, and statements in it may differ from the views of others in AXA Investment Managers.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk , including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested.