CIO Views: Fixed income performance driven by lower rate expectations

- 30 September 2024 (3 min read)

KEY POINTS

Chris Iggo, CIO AXA IM Core

Fixed income benefiting from lower rate expectations

Lower interest rate expectations – further confirmed by the Federal Reserve’s September cut - have helped drive recent strong fixed income performance. Returns for global government and corporate bonds over the third quarter have been among the strongest of the last 10 years. Going forward, bond yields may not be able to fall much further given what is already priced in. For rate expectations to decline further, the narrative would have to be that recessions risks are increasing or that a ‘neutral’ level for rates is even lower than previously thought. However, this is a low conviction view, given that recession signs are minimal so far. Forecasts of rates below 3% in the US and below 2% in Europe by the end of 2025 look to reflect the most likely macroeconomic outcomes.

As such, we believe the best way to access fixed income remains through yield curve steepening strategies, i.e. focusing on bonds towards the shorter end of the maturity spectrum. These should benefit from lower central bank interest rates. Additionally, corporate bonds remain attractive at current yields. Cash interest rates are set to fall below average yields on high grade corporate bonds, while high yield bonds provide a significant yield premium. Fundamentals in the corporate sector are solid and demand for higher yielding, income-generating assets remains strong. A consolidation of yields is not a negative sign for fixed income returns.

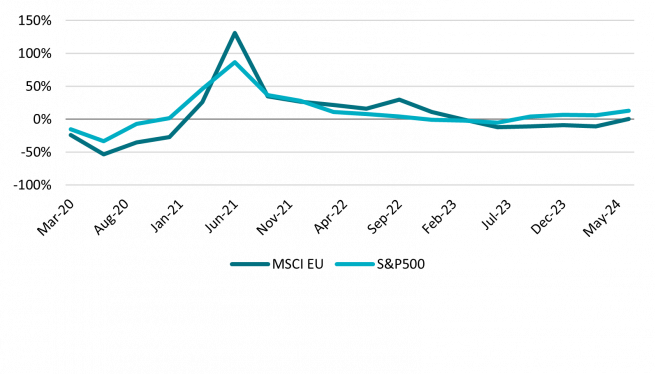

Alessandro Tentori, CIO Europe

European equities: Improved earnings but still lagging the US

Following five quarters of negative earnings growth, European equities have crawled back into positive territory. And data measures suggest markets are bullish on European equities. However, absolute earnings growth still lags Wall Street by a considerable margin. Two factors could explain the 10 times price-to-earnings valuation gap between the MSCI US and MSCI EU indices.

Firstly, structural factors - relatively low productivity, regional fragmentation and implementation issues on European Union (EU) projects – such as the Banking Union - continue to depress Europe’s potential growth rate. The International Monetary Fund expects the US to grow almost twice as fast as Europe in the long run.

Secondly there’s sectoral differences. Looking at the historical composition of major indices, Europe seems to lag in industries like information technology. Some 20 years ago, the sector represented 16% of the S&P 500’s and 4% of the Stoxx 600’s market capitalisation. By the end of 2023, the share had increased to 29% in the US, but only to 7% in Europe. However, industrials and healthcare have gained in importance in the bloc since 2004.

Assuming artificial intelligence-based technology will dominate in the years to come, Europe’s specific industrial make-up might be a key factor both in terms of long-term macroeconomics and expected performance - a crucial issue highlighted by former European Central Bank President Mario Draghi’s recent report on EU competitiveness.

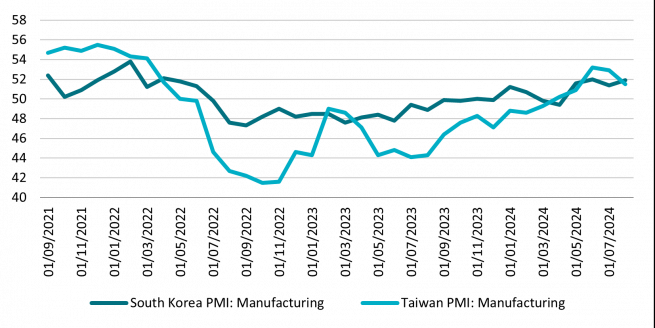

Ecaterina Bigos, CIO Asia ex-Japan

Asia-Pacific manufacturing holding up, powered by AI

Despite worries about artificial intelligence (AI) overhype, US capital goods imports remained robust over the past year, driven by industrial machines, computers, computer accessories and semiconductors - likely due to AI-related investment and spurred on by the 2022 CHIPS act. In contrast, consumer goods imports have largely returned to pre-pandemic levels.

This resilient investment in technology is supporting Asia’s tech trade. The initial winners of the investment cycle have been the enablers – infrastructure firms, storage providers and chipmakers. Asia ex-Japan has the highest share among the major regions of enabler companies, primarily in the semiconductor and hardware supply chain. Taiwan, followed by South Korea, are the market leaders and industry bellwethers.

Taiwan recorded sharp growth in chip exports of 89.8% year on year to September 2024, while South Korea’s rose by 44% over the same period. This has contributed to both countries’ manufacturing Purchasing Managers’ Indices staying resilient despite the global growth slowdown. The drivers are undoubtedly narrow and could be derailed if demand falters, but for now, with under-investing in AI perceived by many

corporates as a bigger risk than over-investing, the cycle likely has further to run.

Asset Class Summary Views

Views expressed reflect CIO team expectations on asset class returns and risks. Traffic lights indicate expected return over a three-to-six-month period relative to long-term observed trends.

| Positive | Neutral | Negative |

|---|

CIO team opinions draw on AXA IM Macro Research and AXA IM investment team views and are not intended as asset allocation advice.

Rates | Easing cycle in full swing but much is already priced in | |

|---|---|---|

US Treasuries | Market already priced for significant rate cuts in 2025 | |

Euro – Core Govt. | Little value right now with ECB rate cuts priced in | |

Euro – Peripherals | Presents opportunities and higher real yields than Bunds | |

UK Gilts | Interest rate cuts fully discounted; markets await fiscal plans | |

JGBs | Uncertainty over Bank of Japan policy normalisation path. Yen remains volatile | |

Inflation | Market pricing not discounting any post-election inflation shock |

Credit | Favourable pricing is increasing the asset class’s contribution to excess returns | |

|---|---|---|

USD Investment Grade | Without significant growth deterioration, credit to remain resilient | |

Euro Investment Grade | Resilient growth and lower interest rates support credit’s income appeal | |

GBP Investment Grade | Returns supported by better growth and expectations of rate cuts | |

USD High Yield | Narrative of growth without inflation is supportive. Fundamentals and funding remain strong | |

Euro High Yield | Strong fundamentals, technical factors and ECB cuts support total returns | |

EM Hard Currency | Higher quality universe, well-placed with US interest rate cuts commencing |

Equities | Soft landing to support stocks into year-end | |

|---|---|---|

US | Lower rates should sustain confidence in earnings | |

Europe | Attractive valuations, along with positive economic and earnings surprises | |

UK | Relatively more attractive valuations and positive economic momentum | |

Japan | Benefitting from semiconductor growth. Reforms and monetary policy in focus for broader performance | |

China | Policy announcements may lead to improved growth and market performance | |

Investment Themes* | Secular spending on technology and automation to support relative outperformance |

*AXA Investment Managers has identified six themes, supported by megatrends, that companies are tapping into which we believe are best placed to navigate the evolving global economy: Technology & Automation, Connected Consumer, Ageing & Lifestyle, Social Prosperity, Energy Transition, Biodiversity.

Disclaimer

This website is published by AXA Investment Managers Australia Ltd (ABN 47 107 346 841 AFSL 273320) (“AXA IM Australia”) and is intended only for professional investors, sophisticated investors and wholesale clients as defined in the Corporations Act 2001 (Cth).

This publication is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Market commentary on the website has been prepared for general informational purposes by the authors, who are part of AXA Investment Managers. This market commentary reflects the views of the authors, and statements in it may differ from the views of others in AXA Investment Managers.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk , including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested.