Record highs, positive sentiment – what could possibly go wrong?

- 13 December 2024 (5 min read)

Investors have been paid for taking risks in 2024. And there will be plenty of risks to consider in 2025 but whether the rewards will be the same is questionable. After two years of super-strong returns, US equity prices are a core element of the outlook for overall market performance. The US market is hitting extreme valuation levels on some measures, which in the past have been followed by negative returns. The post-election euphoria is likely to continue with corporate tax cuts and deregulation to look forward to - and US exceptionalism will remain a theme. But you pay a mighty price to buy the market today. That fact alone demands some consideration of what the risk adjusted expected return could be.

The Stella Artois stock market

In the spirit of 2024 being a stellar year for the S&P 500 index and to reflect the current bullish consensus on equities, I thought I might discuss a topic which is always a point of conversation with clients - valuations. There is an enduring concern that the US can’t possibly maintain its current valuations, and as such, a market crash is potentially somewhere on the horizon. Last week I discussed how US equities had been the best performing asset class since the global financial crisis. Compound annual returns have been around 11% since the early 1970s. However, there have been significant market corrections and some – but not all – have been preceded by extreme valuation levels. We might be close to one now.

No worries

There are several things to consider. One is the level of earnings and how they will evolve and particularly how they will grow in real terms. A second is the multiple of stock prices to earnings, and a third is the level of risk-free yields. Today, earnings for the S&P 500 universe are expected to grow by 14% over the next 12 months, inflation is projected to be around 2.5% and bond yields are forecast to be largely unchanged. No need for concern then. On that basis the market could comfortably reach a level of around 6,500 without valuation metrics materially worsening.

But on some measures…

So what might it take to create the conditions for a significant market adjustment? The methodology developed by the economist Robert Shiller is useful. It attempts to iron out the relationship between equity prices and earnings by adjusting earnings by inflation and the ups and downs of the cycle. I used this basic approach to estimate the five-year cyclically and inflation adjusted price-earnings (CAIPE5) ratio for the S&P 500. It currently stands at 28.4 times compared to the 12-month forward price-to-earnings ratio (PE) of 22.3 times. On my measure, the CAIPE5 has peaked at around 30 times on two previous occasions in the last 34 years – 1999-2000 and in early 2022 on the eve of the most recent Federal Reserve tightening cycle. On both occasions, the market fell, and subsequent equity returns were negative.

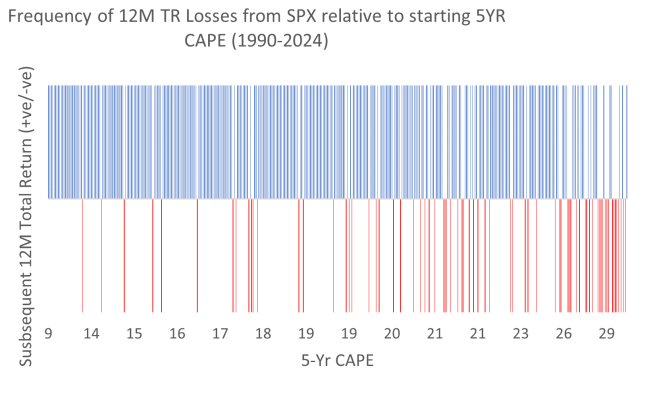

…returns could be challenged

A high PE valuation is not a guarantee of a market correction. However, looking at the S&P 500’s 12-month total return relative to the CAIPE5 at the beginning of each period shows an increased frequency of negative one-year returns, the higher the PE ratio goes. Chart 1 illustrates this. The red bars are negative 12 months returns. They become more obvious as the PE increases (across the x-axis).

Relative yields

Some people like to look at the relative valuation of equities to bonds as another potential marker of negative equity returns ahead. I took the inverse of the CAIPE5 ratio to give an adjusted earnings yield and compared that to the prevailing 10-year bond yield since 1985. Today the adjusted equity yield is marginally below the bond yield – at about 21 basis points (bp). At the time of the 2000 crash, the equity yield was nearly 300bp below the bond yield. Using real bond yields, the gap today is about 220bp (in favour of equities). It was flat in 1999-2000. Using five-year bond yields does not change the picture very much. In 2022, it was the rise in bond yields which caused the equity market to decline. Today, the level of bond yields does not appear to threaten the equity market.

Need to watch bond yields

To get a CAIPE5 of 30 and an earnings yield gap of -300bp, we need some big moves to happen. Expected real earnings growth would need to slow significantly through either reduced earnings expectations or higher inflation than currently expected. This would also mean higher bond yields. In 1999-2000, the CAIPE5 was around 30 times, and bond yields were around 6%. A combination of Donald Trump’s policies could create concerns about higher inflation and higher bond yields and, along with a further increase in the market index price level (the S&P 500 keeps making new highs), conditions could become more vulnerable to a shock. An aggressive asset allocation rotation out of stocks into bonds could be a real surprise in 2025-2026 but it is not in the current consensus outlook.

Technology distortions

I am not forecasting an equity crash. Indeed, our core outlook is still positive on equities, especially US stocks. But I am sure that US stock valuations will remain a core element of discussions amongst finance professionals in 2025. The valuation numbers are clearly distorted by what has happened with technology stocks and there is an even keener focus on the so-called Magnificent 7. Applying the methodology to the S&P 500 Information Technology sector we get a CAPEI5 of 44 times now – it stood at 63 times in January 2000! The equally weighted S&P 500, for which I have less data on earnings on an equally weighted basis, has a CAIPE5 of 24 times today (compared to a recent peak of 28.8 times at the start of 2022). Compared to non-US markets this is still expensive even if it suppresses somewhat the impact of technology stocks.

The earnings rise for leading technology companies reflects an important technological jump with the advent of artificial intelligence (AI) technologies. There is clearly a belief that AI will lead to productivity growth and a stronger US economy. I believe that too. However, as we saw in 2000, not every technology story works out well. Anything that temporarily, questions the AI theme - regulation, technology failure and/or supply chain shocks – could dramatically impact technology sector valuations.

Caution

I said this in relation to credit spreads recently – expensive valuations themselves don’t guarantee negative returns. However, they change the risk. There still needs to be a trigger, and Trump’s policy agenda, the fragile political-economic situation in Europe and China’s struggles to develop economic stimulus could all potentially spur on a deterioration in investor confidence. The S&P 500 has delivered a total return of 35% since the Fed’s last rate hike in July 2023 and looks set to record two consecutive years of more than 25% total return. Given the backdrop, a third might be stretching it. Caution is required.

Holiday times

This is my last note of the year. It has been a very strange one, personally, professionally and as a Manchester United fan. At least markets have delivered positive surprises which has boosted wealth for many people. Away from markets, football has been particularly disappointing. And the state of the world is a worry – more catastrophic climate events, the tragedy of conflict in the Middle East and the intensification of social media absurdity (concerns about an impending Alien attack on New Jersey is the latest bout of hysteria on X). And this quote from Shakespeare’s Richard III seems appropriate when thinking about the never-ending rotation of political charlatans – “and thus I clothe my naked villainy, with old ends stolen forth of holy writ, and seem a saint when most I play the devil”.

But it is the season to remember the good, to spend time with loved ones, to eat and drink well and to celebrate all the intrinsic magic of the human experience. Collectively, most of us will continue to strive to make the world better – reducing environmental damage and addressing social injustice. The financial world can and does do its bit, sharing a desire to build wealth without doing harm. So have a great holiday season and I will be back in January, and we go again in 2025!

(Performance data/data sources: LSEG Workspace DataStream, Bloomberg, AXA IM, as of 12 December 2024, unless otherwise stated). Past performance should not be seen as a guide to future returns.

Disclaimer

This website is published by AXA Investment Managers Australia Ltd (ABN 47 107 346 841 AFSL 273320) (“AXA IM Australia”) and is intended only for professional investors, sophisticated investors and wholesale clients as defined in the Corporations Act 2001 (Cth).

This publication is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Market commentary on the website has been prepared for general informational purposes by the authors, who are part of AXA Investment Managers. This market commentary reflects the views of the authors, and statements in it may differ from the views of others in AXA Investment Managers.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk , including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested.